A big cash down payment often stops people from getting the car they need—but what if you could skip it altogether? With the right financing strategy, it’s possible to drive off the lot with $0 down. These offers are more common than you think and available to many types of buyers—not just those with perfect credit.

Zero-down deals can be tempting, but knowing when they truly benefit you—and how to avoid getting stuck with hidden costs—can make all the difference.

WHAT IS A “$0 DOWN”?

In car financing, “$0 down” typically means you’re not making a down payment toward the vehicle’s price at signing. However, this does not always mean “no money due at all.”

Here’s how it usually breaks down:

- No down payment is required (the portion that reduces your loan amount)

- Taxes, title, license, registration, and doc fees may still be due at signing

- In some promotions, “$0 due at signing” includes all of the above—but this applies mostly to leases or very specific finance deals for well-qualified buyers

✅ Clarification: Most buyers will still need to pay government-mandated fees and sales tax unless those are explicitly rolled into the loan or waived through promotions.

IS A $0 DOWN CAR DEAL LEGIT?

Zero-down financing is both real and commonly offered—particularly during special promotions or by lenders willing to cover the entire cost of the transaction.

However, whether you qualify—and how favorable the terms are—depends on several factors:

- Your credit score and credit history

- Income verification

- Vehicle selection and lender guidelines

- Loan-to-value (LTV) ratio: The total loan amount vs. the car’s actual value

Lenders calculate risk based on these inputs. Financing the entire cost of the car, including taxes and fees, increases risk—so expect more scrutiny or higher interest if you don’t make a down payment.

WHAT ARE THE PROS & CONS OF $0 DOWN?

✅ Advantages:

- No large upfront cost — You keep your savings for other expenses

- Faster purchase process – You don’t need time to save for a down payment

- Useful for emergencies — Ideal if your car was totaled, stolen, or you urgently need transportation

- Builds credit — As long as you make on-time payments, your auto loan can improve your credit history

❌ Disadvantages:

- Higher monthly payments — You’re financing a bigger amount

- More total interest paid — Especially if you choose a longer-term loan

- Risk of negative equity — You may owe more than the car is worth in the early months of the loan (known as being “upside down”)

- Limited qualification — Offers are often reserved for buyers with decent to strong credit

MORE: Explore the Credit Score Required to Buy a Car

WHO QUALIFIES FOR $0 DOWN CAR LOANS?

Contrary to popular belief, you don’t need perfect credit to qualify. However, the better your financial profile, the easier it will be to get approved without needing cash up front.

Here’s what most lenders consider:

✅ Stronger Applicants (Easiest Approval):

Buyers in this category usually have a clean credit history and strong financial footing. Dealerships and Lenders view these borrowers as low-risk, making them ideal candidates for $0 down programs—often with favorable terms like low interest rates or shorter loan durations.

These buyers typically have:

- Credit score of 670 or higher (Prime or Super Prime tier)

- Low debt-to-income ratio (DTI), showing manageable financial obligations

- Stable, verifiable employment, often with several years at the same job

- Previous auto loan history with on-time payments or an existing paid-off car loan

They are the most likely to be approved for true $0 down financing, including offers that roll taxes and fees into the loan.

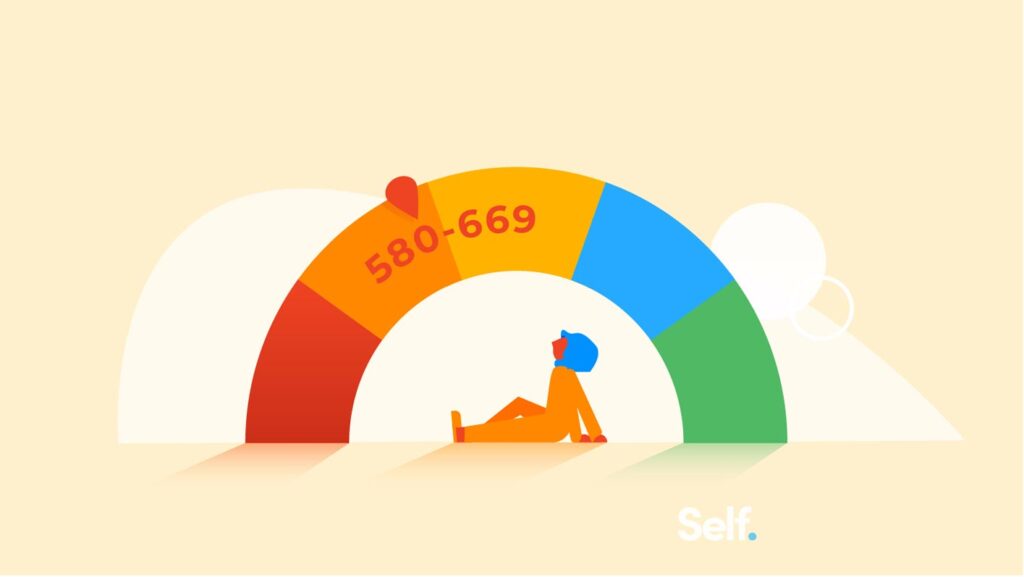

🟡 Moderate Credit (Possible Approval):

Buyers in this range – typically between 580 and 669 – may not have perfect credit, but their financial behavior shows promise. They might have had a late payment in the past or carry higher debt loads—but they’re not considered high risk.

Lenders may still offer $0 down to these borrowers, especially if they’re able to:

- Provide proof of steady income

- Offer trade-in equity to reduce the loan amount

- Finance a less expensive vehicle

- Agree to slightly higher interest rates or longer loan terms

These buyers might also be approved with conditions, such as a co-signer or a small upfront payment to cover fees.

🔴 Subprime Credit (Approval with Conditions):

Buyers with lower credit scores—typically under 580—are often considered subprime or high-risk borrowers. While $0 down is harder to get in this tier, it’s not impossible. Many dealerships, especially those with special finance programs or in-house financing (like Buy Here Pay Here), work with subprime lenders to offer flexible options.

However, expect to:

- Pay higher interest rates (often 15% or more)

- Be limited to certain vehicles, usually older or lower-priced models

- Provide extensive documentation, including proof of residence, income, references, and sometimes insurance verification

- Potentially need a co-signer or trade-in vehicle to offset the lack of a down payment

Some subprime lenders may approve zero-down loans by adjusting the terms to account for the higher risk, such as shortening the loan duration or increasing the monthly payment.

💡 Important: Always confirm that the lender reports your payments to the major credit bureaus. This is crucial if you’re using the loan to rebuild your credit over time.

MORE: Learn How to Buy a Car with Bad Credit

WHERE TO FIND ZERO DOWN CAR LOAN?

1. Franchise Dealership Promotions

Franchise dealerships (those affiliated with major automakers like Toyota, Honda, Ford, Hyundai, and others) frequently run promotional events offering $0 down as part of a larger sales campaign. These offers are often seasonal or tied to specific sales periods like holiday weekends, end-of-year clearance events, or new model releases.

What to know:

- These deals are usually available only to well-qualified buyers with strong credit scores (typically 660+).

- Even if the ad says “$0 down,” the offer may still require you to pay taxes, title, and registration unless explicitly stated otherwise.

- Promotions may be limited to specific vehicles, such as entry-level trims, older inventory, or models the dealership is trying to move quickly.

Franchise dealers can offer flexible lender options, especially if you’re pre-approved or trading in a vehicle with equity.

2. Manufacturer-Sponsored Programs

Automakers themselves often run nationwide $0 down financing or lease specials through their captive financing companies (e.g., Toyota Financial Services, Ford Credit, Honda Financial Services). These deals are usually advertised online and through local dealers, often during promotional events.

What to know:

- Lease deals may advertise “$0 due at signing”, which can cover everything—including your first payment, security deposit, and registration—but only for top-tier credit customers.

- Purchase offers with $0 down are less common than lease specials, but they do exist, often paired with low-APR financing or cash-back incentives.

- Approval requires excellent credit, often 700+, and verifiable income.

These offers are ideal if you want a new vehicle with full warranty coverage, low maintenance costs, and the flexibility of a lease.

3. Credit Unions and Local Banks

Many California-based credit unions, such as Golden 1 Credit Union, SchoolsFirst FCU, and Patelco, offer zero-down auto loans for members in good standing. Unlike dealer promotions, these offers are often available year-round and may come with lower interest rates and fewer restrictions.

What to know:

- You typically need to be a member of the credit union, but membership is often open to anyone who lives or works in certain counties.

- Credit unions evaluate more than just your credit score—they also consider your overall banking relationship and financial behavior.

- Many allow you to finance taxes, registration, and fees into the loan, making true $0 out-of-pocket possible.

Credit unions are a smart choice for buyers with good credit who want personalized service and transparent lending terms.

4. Buy Here Pay Here Dealerships (BHPH)

Buy Here Pay Here dealerships offer in-house financing, meaning the dealer itself acts as the lender. These dealerships often advertise $0 down and guaranteed approval, especially for buyers with poor or no credit.

What to know:

- These dealerships usually don’t require credit checks, making them appealing to buyers with recent bankruptcies, repossessions, or low scores.

- Interest rates are typically much higher than traditional lenders—sometimes exceeding 20% APR.

- You may be required to make weekly or bi-weekly payments, and the selection of vehicles is often limited to older models.

- Some BHPH dealers do not report payments to credit bureaus, which means your on-time payments may not help rebuild your credit.

BHPH dealers can be a useful short-term solution for buyers in tough situations, but it’s important to read the fine print and confirm that the loan terms are manageable.

MORE: Explore the Best Time to Purchase a Car

HOW TO QUALIFY & APPLY FOR $0 DOWN FINANCING?

Here’s how to improve your approval chances:

- Check Your Credit Score – Use free services like Credit Karma or check directly with Experian, TransUnion, or Equifax.

- Get Pre-Qualified – Pre-qualification shows what you’re eligible for, without affecting your credit. It also gives you negotiation leverage at the dealership.

- Have Documents Ready:

- Income (recent pay stubs or bank statements)

- Insurance

- Residence

- Employment

- Use Trade-In Equity Wisely – If your current car has equity, this can reduce the amount financed, even if you put no cash down.

- Consider a Co-Signer – A strong co-signer can dramatically improve your loan terms and approval odds.

MORE: Here’s How to Get a Car Loan With No Credit History

FINAL THOUGHTS:

If your priority is low upfront cost and you’re confident in your ability to handle monthly payments, a $0 down car loan or lease can be a smart choice. But you must understand the trade-offs:

- You’ll likely pay more over time

- You may be restricted to certain vehicles or lenders

- Your credit profile plays a major role in eligibility

Do your research, understand the terms, and don’t be afraid to walk away from a deal that doesn’t feel right.

FREQUENTLY ASKED QUESTIONS:

Can I refinance a $0 down auto loan later?

Yes. If your credit improves, refinancing can help lower your interest rate and monthly payment. Just check for prepayment penalties in your original loan.

Can I trade in a car I still owe money on and get $0 down?

If your trade has positive equity, it can help cover the down payment. If you’re upside down, the negative equity may need to be rolled into your new loan.

Will applying for multiple $0 down loans hurt my credit?

If done within a 14–45 day window, multiple inquiries count as one. Use soft credit pull pre-approvals when possible to avoid impact.

Does $0 down impact my car insurance?

Not directly. But full coverage is required for financed cars, and some lenders may require GAP insurance to protect against negative equity.