In Orange County, owning a car isn’t optional for most people—it’s essential. If your credit falls in the subprime range, getting approved for an auto loan is still very possible.

The real risk isn’t approval—it’s ending up in a loan that quietly sets you back financially through high interest, long terms, and hidden trade-offs.

This guide breaks down how subprime auto loans actually work, what OC buyers should realistically expect, and how to protect yourself—while still getting the car you need.

WHAT “SUBPRIME” MEANS

A subprime auto loan typically applies to buyers with lower credit scores or limited credit history. “Subprime” doesn’t mean you’re irresponsible—it means lenders view your profile as higher risk, so they price the loan higher (APR), require more verification, and may limit terms.

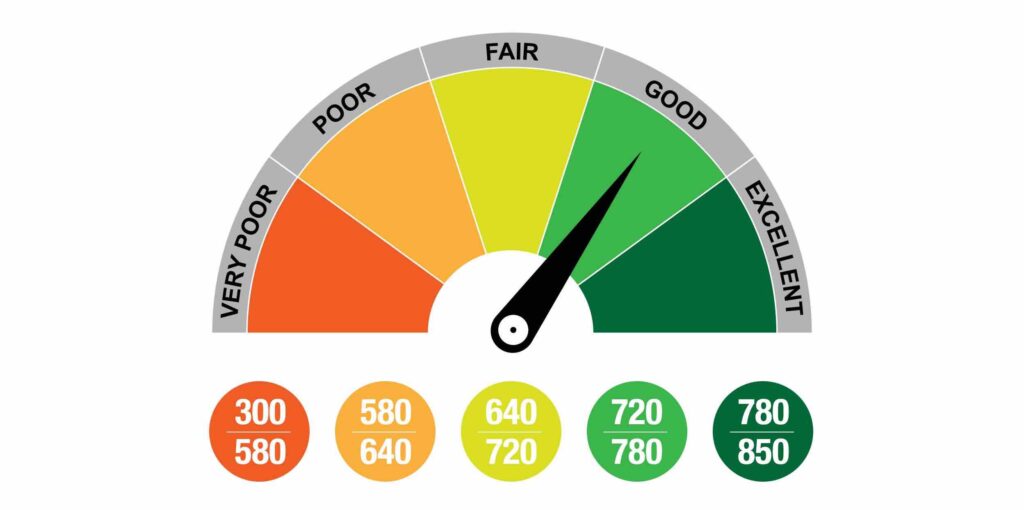

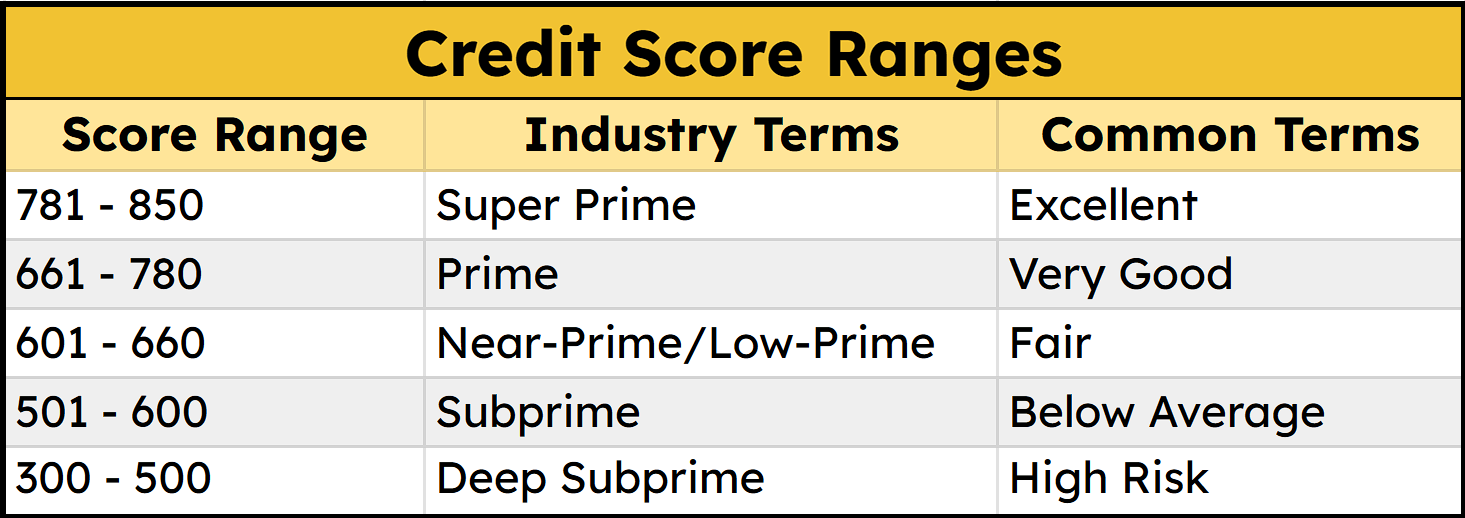

In auto lending, “subprime” is often used as a broad category ranging credit scores from 300-600, but it’s commonly broken down further by credit tier. Based on VantageScore® 4.0, credit tiers generally fall into the following ranges:

Credit score tiers vary by lender, loan type, and scoring model. Ranges shown are approximate for educational purposes.

Being subprime does not mean you can’t buy a reliable car or improve your situation—it simply means the loan structure matters more than ever.

⚠️ INTEREST RATE DRIVES TOTAL COST

Many buyers naturally focus on the monthly payment. That’s understandable—but with subprime loans, the interest rate is often the biggest cost driver.

- Subprime APRs are significantly higher than prime rates.

- Auto loans are amortized, meaning early payments go mostly toward interest—which is especially costly when APRs are high.

- Longer loan terms reduce the payment but dramatically increase total cost, especially at higher APRs.

A difference of just a few percentage points in APR can mean thousands of dollars over the life of the loan—even if the monthly payment only changes slightly.

For example, stretching a loan from 48 to 72 months at subprime APRs can add several thousand dollars in interest—even if the payment feels manageable on paper.

📍 MORE: Learn more about how interest rates affect your monthly payments.

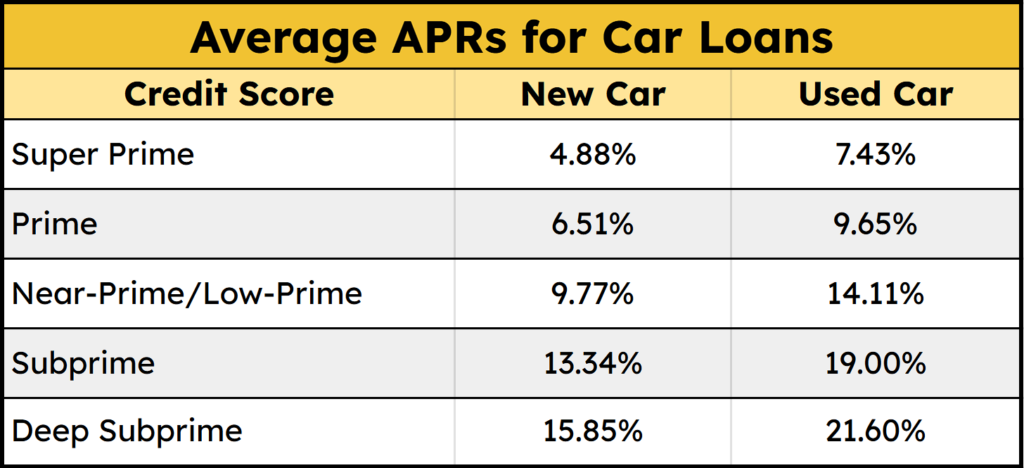

TYPICAL SUBPRIME AUTO LOAN RATES IN 2025

Rates vary by lender and borrower profile, but it helps to anchor expectations with reputable market data.

Experian’s reported average APRs by credit tier (VantageScore 4.0) show how sharply rates jump as credit drops.

Source: Experian State of the Automotive Finance Market, Q3 2025

Notice how used-car APRs in subprime tiers can approach or even exceed 20%, where interest becomes a dominant portion of the total loan cost.

Used vehicles typically carry higher APRs than new cars, and when combined with longer loan terms, this can significantly increase the total amount of interest paid.

⛔ BIGGEST MISTAKES SUBPRIME BUYERS MAKE

Avoiding these mistakes will put you ahead of most buyers:

1. Shopping Only By Monthly Payment

A low payment can hide a long loan term and excessive interest. Always look at:

- APR

- Loan Length

- Total Amount Paid Over Time

A dealer can make almost any car “fit” by stretching the term. A lower payment often means a higher total cost — especially at subprime APRs.

2. Rolling Everything Into The Loan

Optional add-ons like service contracts, GAP waivers, and other products are often financed as a lump sum and paid over the whole loan term—meaning you pay interest on them too. Some can be useful—but they should never be automatic.

3. Taking the First Approval Without Comparing Options

Even subprime buyers can often qualify with multiple lenders, and small APR differences can make a meaningful impact.

With subprime loans, even a slight rate improvement can translate into real savings, so rate shopping is not optional, it is essential. In subprime financing, details matter — and small differences can cost thousands.

📍 MORE: How to Own a Car With Bad Credit.

🔍 WHAT LENDERS CARE ABOUT

Credit score matters, but approvals often hinge on your stability and your ability to repay.

Common factors lenders look at include:

- Income & job stability (consistent pay is powerful)

- Debt-to-income (DTI) (how much of your income is already committed)

- Down payment / loan-to-value (LTV) (more down = less lender risk)

- Residence stability

- Vehicle factors (age, mileage, and book value)

Lenders are assessing risk, not judging you — the goal is to see whether the loan fits your financial reality.

In Orange County, where rent and cost of living are high, showing stable income, manageable DTI, and even a modest down payment can significantly improve both approval odds and APR terms.

✅ A SMART SUBPRIME STRATEGY

Here’s the approach that consistently produces the best outcomes for subprime buyers:

Step 1: Get Pre-Approved Before You Shop

Even if you plan to finance at the dealer, a pre-approval will gives you:

- A realistic rate baseline

- A spending limit

- Negotiation leverage

Pre-approval doesn’t lock you in — it simply gives you a benchmark to compare against dealer offers.

👉 Get pre-approved before you walk into the dealership — it changes the entire conversation.

Step 2: Choose the Right Car, Not Just the Right Payment

Subprime buyers should prioritize vehicles that reduce lender risk and avoid costly repairs.

The car you choose directly affects your approval, interest rate, and long-term ownership cost.

Strong general targets:

- Reliable, widely available models (lower repair costs and easier approvals)

- Clean-title vehicles with verifiable history

- Models with widely available parts/repair support

- Lower mileage (reduces lender risk and future repair exposure)

📍 MORE: Best Reliable, Budget-Friendly SUVs for Subprime Buyers.

Step 3: Set Guardrails, Not Just a Goal

Before you start shopping, set clear financial limits so you know exactly what you can afford and avoid stretching your budget.

- Loan Term: What’s the longest you’re willing to finance? (avoid 84 months if possible)

- Monthly Payment: What can you comfortably afford each month?

- Total Budget: Your true budget isn’t just the loan — it’s the total cost of owning the car.

- Insurance

- Fuel

- Maintenance

Setting these guardrails before you shop helps you stay in control of the deal — instead of letting the deal define your budget.

HOW SUBPRIME BUYERS CAN IMPROVE THEIR SITUATION

A subprime loan doesn’t have to be permanent — the goal is to use it as a stepping stone to better terms.

The Fastest Levers You Can Pull:

- Put more down (even $500–$2,000 can change LTV and terms)

- Choose a cheaper car (borrowing less saves interest on every payment)

- Shorten the term when possible (less time = less interest)

- Add a qualified co-signer (only if it’s a solid, trusted agreement)

- Refinance after 6–18 months if you’ve made consistent on-time payments and your credit profile has improved

Even a modest refinance can significantly reduce your remaining interest and lower your monthly payment.

📍 MORE: Contact Us to review your options and see what you may qualify for — including whether refinancing could lower your rate over time.

FINAL THOUGHTS:

Buying a car with subprime credit isn’t about finding any approval — it’s about making a smart decision that sets you up for better terms over time.

Focus on the total cost, choose the right vehicle, and structure your loan with intention. Small decisions today can make a big difference in what you pay — and how quickly you improve your situation.

👉 Take your time, ask the right questions, and make sure the deal works for you — not just now, but long-term.