Buying a car is a major milestone—but what if you have no credit history? Many people, especially students, recent immigrants, or young professionals, face this exact situation. The good news? Yes, you can get a car loan with no credit. But it helps to understand the process, your options, and how to set yourself up for success.

In this guide, we’ll break down how car loans work for people with no credit, what lenders look for, how to improve your approval odds, and how to avoid costly mistakes.

WHAT DOES “NO CREDIT” ACTUALLY MEAN?

If you’ve never taken out a loan, used a credit card, or had any credit accounts reported to the major bureaus (Experian, Equifax, and TransUnion), you likely have no credit history—also called being “credit invisible.” This isn’t the same as having bad credit, but it still makes lenders nervous because they don’t know how you’ll handle repayment.

Lenders view this as a risk not because you’ve done something wrong—but because they have no data to base their decision on. It’s like hiring someone with no resume.

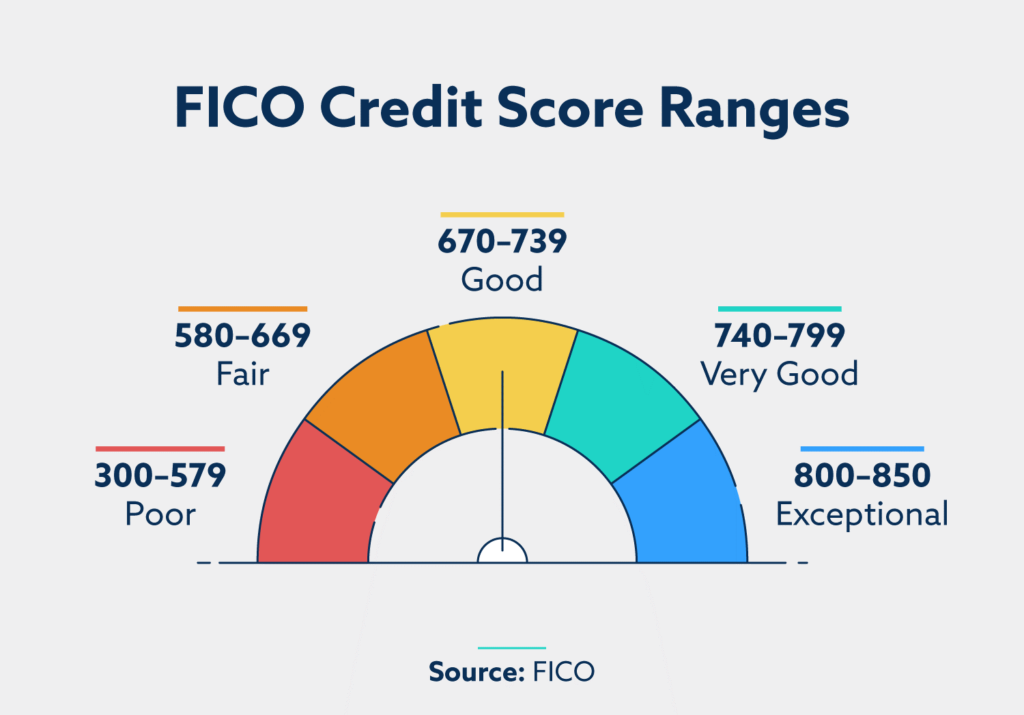

🔍 Pro Tip: A FICO score isn’t generated until you’ve had at least one credit account open and active for six months.

CAN YOU STILL GET A CAR LOAN WITHOUT CREDIT?

Yes, but it may take a bit more work. Since lenders base most loan decisions on your credit profile, having no credit means they need to look at other indicators of risk. That could include:

- Proof of stable income

- Employment history

- Debt-to-income (DTI) ratio

- Down payment amount

- Co-signer availability

Lenders want assurance you can make monthly payments consistently—even without a credit track record.

Insider Tip: Many lenders use alternative data such as rent payments, utility bills, or even recurring subscription payments to assess creditworthiness for first-time borrowers.

💡 7 SMART WAYS TO GET APPROVED FOR A CAR LOAN WITH NO CREDIT

Here’s how to boost your chances of getting approved:

1. Show Strong Proof of Income

Lenders want to be sure you can repay the loan. Consistent income is one of the most powerful trust signals you can offer.

What to do:

- Provide at least 2–3 months of pay stubs or direct deposit statements.

- Bring W-2s or tax returns for the past two years.

- If you’re self-employed or a gig worker, show 1099s, monthly revenue reports, or accounting software summaries.

🧾 Consistency matters more than a high income. Even modest earnings from a reliable job can demonstrate stability.

2. Make a Larger Down Payment

A down payment does two things: it shows you’re financially committed and reduces the amount you need to borrow.

Why it helps:

- Lowers your monthly payment.

- Reduces the lender’s risk.

- Improves your loan-to-value (LTV) ratio—making your loan application more attractive.

How much is enough?

- Aim for at least 10%, but 20% is ideal.

- Even a $1,000–$2,000 down payment can make a big difference on used cars.

💡 The more you put down, the more negotiating power you’ll have on loan terms.

3. Consider a Co-Signer

A co-signer is someone with established credit who agrees to back your loan. They are legally responsible if you fail to pay.

Who makes a good co-signer?

- Parents, close relatives, or a spouse with a strong credit profile.

- Someone with a FICO score of 700+ who trusts your financial responsibility.

Benefits:

- Better interest rate.

- Higher loan approval likelihood.

- Greater flexibility on loan term and vehicle choice.

Risks:

- Missed payments hurt both your and their credit.

- It can strain personal relationships if expectations aren’t clearly defined.

📘 Tip: Put everything in writing. Agree on communication, payments, and what to do if financial issues arise.

4. Start with a Credit Union or Local Bank

Local credit unions often work closely with members to approve first-time auto buyers.

Advantages:

- Lower interest rates than commercial banks.

- More lenient underwriting.

- Personalized service from a loan officer.

How to prepare:

- Become a member before applying.

- Ask about special programs like “first-time auto buyer loans.”

- Prepare all financial documents to present to a loan officer.

🏦 Many credit unions allow non-profit or community-based memberships, even for students or new residents.

5. Explore In-House Financing at Dealerships

Some dealerships offer internal financing or work with subprime lenders who approve buyers without traditional credit.

Common options:

- Buy Here, Pay Here (BHPH)

- Special finance programs through lenders like Credit Acceptance or Westlake Financial

Pros:

- Quick approval, even with no credit.

- Vehicle and financing from one source.

Cons:

- Higher interest rates (often 15%+).

- May not report to credit bureaus.

- Risk of repossession if you miss payments.

🚫 Avoid BHPH if your goal is to build credit. Always ask if the dealer reports payments to the credit bureaus.

6. Limit the Loan Amount

Your first car doesn’t need to be expensive—it needs to be reliable and budget-friendly.

Tips for smart vehicle selection:

- Look for used cars under $10,000 with good safety and reliability scores (Toyota Corolla, Honda Civic, Ford Focus).

- Check the total cost of ownership (insurance, gas, maintenance).

- Use online marketplaces to compare prices before stepping into a dealership.

Rule of thumb:

- Keep your monthly car payment under 10% of your monthly income.

- Aim for a loan term of no more than 48–60 months.

📉 A smaller loan not only helps with approval—it also reduces your financial stress over time.

MORE: Vehicles that Have the Highest Resale Value

7. Get Pre-Qualified

Before visiting a dealership, get pre-qualified for a loan through the website, online lenders, or your bank.

Why it matters:

- Shows you’re a serious buyer.

- Gives you leverage during negotiations.

- Helps you avoid inflated dealership interest rates.

What you’ll need:

- Your personal info (name, address, SSN).

- Income and employment details.

- Estimated vehicle price and down payment.

Top platforms:

🔍 Pre-qualification uses a soft credit check and won’t affect your credit score. It’s a risk-free way to explore your loan options.

WHAT KIND OF INTEREST RATES SHOULD YOU EXPECT?

Without credit, your interest rate will likely be higher than someone with good credit. While prime borrowers might see rates around 5–6%, borrowers with no credit may face rates from 9% to 20% depending on the lender and terms.

Use online calculators to estimate your monthly payment with different loan terms and rates.

Tip: Even if you start with a high rate, you can refinance your car loan later—once you’ve built credit with on-time payments.

MORE: Best Time to Buy a Used Car

DOCUMENTS YOU WILL LIKELY NEED

To strengthen your loan application, bring the following documents when applying:

- Valid driver’s license

- Proof of income (pay stubs, bank statements)

- Proof of residence (utility bill, lease agreement)

- Personal references

- Vehicle insurance details

- Down payment (cash, check, or trade-in title)

Having these ready shows you’re prepared and responsible, which helps build trust with the lender.

⚠️ WATCH OUT FOR THESE RED FLAGS

When you’re a first-time borrower with no credit, some lenders may try to take advantage. Be cautious of:

- Extremely high interest rates (above 20%)

- Hidden fees or prepayment penalties

- Balloon payments or overly long loan terms (72+ months)

- Dealers pushing you into cars beyond your budget

🚨 Always read the fine print. If something feels off, it probably is. Don’t be pressured into signing on the spot.

CAN A CAR LOAN HELP YOU BUILD CREDIT?

Absolutely. In fact, a car loan is one of the best ways to start building credit—if you make on-time payments every month. Your lender will likely report your activity to the credit bureaus, and after 6–12 months of consistent payments, you’ll start generating a positive credit history.

Also, consider signing up for free credit monitoring tools like Credit Karma or Experian Boost to track your progress

🛠️ Build Your Credit Tip: Ask the lender if they report to all three major credit bureaus. Some smaller lenders or BHPH dealerships may not.

WAITING vs. PURCHASING

It depends on your situation. If you can wait a few months, consider getting a secured credit card, using it responsibly, and building a small credit history. But if a car is urgent for work or school, following the tips above can still lead to a good outcome.

Even 3–6 months of positive payment history on a small account can help you qualify for better rates.

MORE: Know These Types of Used Cars Before You Choose

✅ CONCLUSION

Having no credit doesn’t mean you’re out of options—it just means you’ll need to be strategic. Focus on showing financial responsibility through income, down payment, and documentation. Whether you go with a credit union, bank, or dealership, you can get the keys to your next car and start building your credit one payment at a time.

📈 This first auto loan could be your stepping stone to building strong credit, qualifying for lower rates in the future, and achieving bigger financial goals.